Remember the huge Silicon Valley tech boom of the 1990s? Many startups transformed into giant corporations, while ESOP was one of the key tools they used to support their growth. This model, where employees get a real stake in the companies they help grow, is not new. But how does this traditional, equity model of ESOP apply in the context of the Czech business environment?

In the Czech Republic, we can observe an increased interest in equity ESOPs, especially in technology startups and medium-sized companies that are looking for ways to motivate and reward their key employees. But what are the legal nuances that we can encounter in the Czech context? And why should companies opt for this traditional model when there are many modern alternatives?

In today’s article we will take a closer look at the standard equity model of ESOP, its advantages, and the challenges and specifics of its application in the Czech Republic. Anyone involved in business or people management will find this insight into this traditional motivation and reward tool extremely useful.

Basic definitions and types of equity ESOPs

The basic characteristic of traditional ESOPs is that the participant acquires an ownership interest in the company under the ESOP (and in accordance with its terms). Thus, the ESOP participant will actually (in the true sense of the word) receive shares in the company from the company.

The equity ESOP has evolved over time and today there are several modifications. We will address the most prevalent ones, which we will discuss below, specifically:

Standard option plan

Direct sale of shares

Employee company

ESOP as a security

Regarding the form on which ESOP is based (company-designed ESOP plan / ESOP agreement), in this regard we refer to our recent blog on virtual ESOPs. In this respect, the form of standard ESOPs does not in fact differ from virtual ones.

1. Standard option plan

Under a standard (equity) ESOP, the ESOP participant acquires options (i.e., the right) to purchase shares (a certain % of shares – Grant Size) in the company at an agreed-upon price (Strike Price), subject to certain conditions for Vesting. (See our previous blog for more detailed information on the terms below.)

The procedure for implementing a standard option plan is typically as follows:

Option Grant – An agreement is entered into regarding the ESOP, under which the ESOP participant is promised to receive an option right to shares in the company if certain conditions are met.

Vesting – The ESOP participant gradually acquires the promised options, and at the end of the vesting period (i.e., the agreed-upon period during which the option right is triggered) the ESOP participant is entitled to the options in full (grant size). Similarly to the virtual ESOP, the concept of Good Leaver / Bad Leaver is applied when an ESOP participant leaves the company, and the entitlement to the option may be linked to the fulfilment of additional conditions (work performance, etc.).

Exercise – Upon completion of the vesting period and, where applicable, fulfilment of other conditions, the ESOP participant may elect to exercise his or her option and acquire shares in the company at an agreed purchase price. In most cases, the exercise of the option is automatic and the participant acquires an ownership interest in the company once the conditions are met.

Exit – In the case of an exit event (e.g., sale of the company to a third party), the ESOP participant sells his or her shares, ideally at a substantially higher purchase price than the price for which he or she acquired it (which is indeed the essence of the equity ESOP).

Since the ESOP participant becomes a member/shareholder of the company upon the exercise of his/her option right, he/she usually also accedes to the company shareholders’ agreement. This is an important difference from a virtual ESOP, where the participant does not have the rights of a shareholder and therefore does not participate in the operation of the company.

An important aspect of equity ESOPs (also applicable to the other types listed below) is the creation of a special type of shares that are then offered to participants. These special shares often lack the right to vote at the general meeting and the right to dividends.

A big misconception among the general startup public is that these participants do not have the right to participate in the general meeting (even if their shares do not carry voting rights) or the right to information.

There indeed exist fundamental rights of which a share cannot be deprived. Those rights include the two rights mentioned. It is therefore important to bear in mind that if you give participants a direct shareholding in the company, you are likely to meet them at general meetings where strategic company matters are discussed which the participants should not or do not need to know. The same applies to the right to information and access to the company’s financial documents.

At the same time, it is necessary to lay down the rules for the disposal (transfer) of these employee shares, e.g. to restrict (or to completely exclude) their transferability and to set the conditions for the forced sale of the employee shares upon exit so that no participant can defeat this sale. However, the degree of risk associated with the possible reluctance of participants to transfer their employee shares cannot be completely eliminated in the case of equity ESOPs.

2. Direct sale of shares

This is a modification of a traditional stock option plan whereby the ESOP participant acquires an ownership interest in the company without the need for vesting (and typically without meeting other conditions). It is therefore not a pure stock option plan. It is really just a case of the company offering a stake in the company to a key employee or other associate who decides to buy it from the company, or receives it from the founders for free.

This type of ESOP is mainly used for the top key employees or associates of the company (chief officers of the company, etc.), or participants who hold important know-how, copyright (e.g. part of an important program) and without whom it would be very difficult or even impossible to continue development. In such a case, it is appropriate to proceed to offer a direct equity stake.

Similar to a traditional ESOP, a participant in a direct ESOP becomes a member/shareholder of the company and therefore usually also accedes to the company shareholders’ agreement.

As far as the implementation process is concerned, it is simpler just like in the case of traditional ESOPs. A participant sells their share(s) together with the other shareholders in the sale of the company.

A common occurrence in this type of ESOPs is also a Reverse Vesting agreement – you can find the definition of this term in one of our previous blogs.

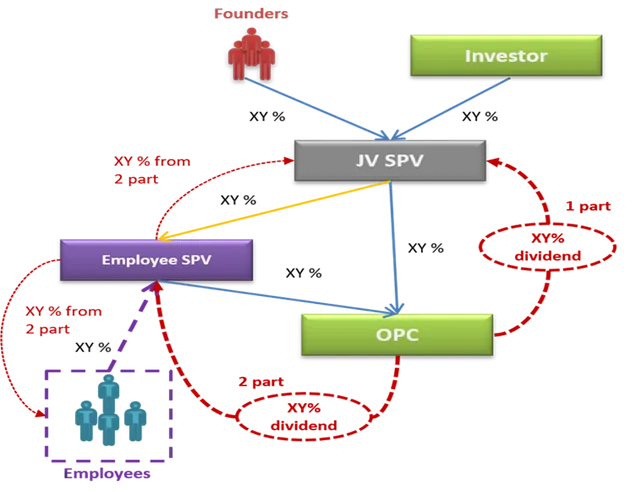

3. Employee SPVs

The last modification of the traditional option plan is the so-called employee SPV (Special Purpose Vehicle). This involves the formation of an employee SPV (i.e., a business company, typically a limited liability company) in which some of the shares are held by ESOP participants.

Hence, an employee SPV has two types of shares. One type is held by ESOP participants, and the other type is held by the founders. Therefore, there is a need for the founders (or some of them) to enter into the employee SPV and exercise control and management functions in it.

The employee SPV then has a direct stake in the company (startup) equal to the ESOP Pool, where the ESOP Pool is distributed to the participants within the employee SPV.

The following example illustrates a model employee SPV:

4. ESOP as a security

Another form of a quasi-virtual ESOP involves warrants, i.e. securities that contain an option to receive a bonus component or to acquire an equity interest in the company.

This is the form that is most prevalent in large corporations, but you do not see it much in venture capital. Rather than being a special type, it is simply another form of embedding ESOP terms in a security that is then issued by the company.

This instrument may have the advantage of being transferable to another participant, should the ESOP terms and conditions allow that.

Advantages and disadvantages of traditional ESOPs

When evaluating the advantages and disadvantages of traditional ESOPs, a comparison with virtual ESOPs is necessary. It is difficult to define some facts only as an advantage or disadvantage, because it is crucial whether we look at the aspect from the perspective of the participant or the company. We will therefore try to outline the advantages and disadvantages by the following breakdown:

Advantages of an equity ESOP for participants:

Equity participation in the company: the participant actually owns a stake in the company, which can reinforce a sense of belonging and commitment to the company. The participant thus works on “his own” and has a real ownership feeling.

Financial advantages: In the case of a successful sale or another liquidation event, the participant may receive a considerable financial benefit.

Voting rights and participation in the operations of the company: In some equity ESOP models, employees may have voting rights associated with their shareholding. However, this is rather sporadic.

Disadvantages of an equity ESOP for participants:

Liquidity: Shares or interests in the company may not be readily marketable (or cannot be sold outside of a liquidation (exit) event), which may limit an employee’s ability to quickly realise gains.

Risk of loss: If the company fails, the value of the shares may fall, leading to financial losses for employees.

Advantages of an equity ESOP for the company:

Employee motivation: True ownership can significantly motivate employees to perform better and be more committed to the company.

Retaining key talent: By offering a stake in the company, the company can better retain key employees.

Improving company culture: Ownership can strengthen the sense of belonging and team spirit among employees.

Disadvantages of an equity ESOP for the company:

Dilution of shares: Employee shares dilute the ownership structure.

Heavier administrative burden: To administer an equity ESOP can be more complicated than a virtual model, especially with respect to voting rights, dividend payments, etc.

Potential conflicts of interest: Employees who have now become shareholders may have different views than the original shareholders on the strategy and future direction of the company.

Conclusion

Equity ESOPs represent a fascinating tool that can have a transformative impact on corporate culture and employee motivation. By offering a real ownership stake in the company, a business can build deeper relationships with those who invest their time and energy in it.

Although an equity ESOP may bring about complications that require diligent management, its potential to strengthen team cohesion and achieve long-term success is unquestionable. For any company which contemplates implementing such a plan, it is important to weigh the pros and cons and tailor the model to its unique needs. Ultimately, equity ESOPs can be the key to rewarding and recognising those who play a crucial role in a company’s success.

Our next blog will cover tax aspects of ESOPs. We hope you will find it equally beneficial.

Did you like this article?

We will be happy to send you other related articles directly to your e-mail.

In respect of business and corporate structure, it is essential to constantly monitor and evaluate the impact of tax policy on the various aspects of corporate decision-making. One of the key tools that is gaining popularity in the Czech Republic is the ESOP system. Although ESOPs can provide many b

Virtual ESOP in the Czech Republic, or when shares remain in the shade. Imagine a world where you can offer employees a share in the company’s success without having to become actual co-owners. A world where remuneration is transparent and performance-based, but without a complex share transfer proc

The history of companies, especially those that have changed the world, is full of stories of employees who became millionaires thanks to shareholdings in the company. An example is Microsoft, which generated approximately 12,000 millionaires in its first ten years. How did they achieve this success

ESOP, option share, virtual share or share option plan - have you heard these or similar terms in the start-up world? These terms probably sound familiar to any founder, employee or investor, but do we really know what lies beneath them? Is it a shareholding in a company, a share in the profits, or